From: James Pierlot

To: Ontario Ministry of Finance

Date: February 11, 2021

Re: Ontario’s Pension Benefits Guarantee Fund: A Practical Way Forward

The only sub-national pension guarantee fund in the world, Ontario’s Pension Benefits Guarantee Fund (PBGF) has survived 40 years, providing a limited guarantee for Ontario members of some underfunded defined benefit (DB) pension with insolvent sponsors.

The PBGF guaranteed pensions up to $1,000 per month until 2018, when the maximum was increased to $1,500. Employer-paid PBGF premiums, initially $1 per member plus 0.2 percent of a solvency deficiency, were increased in 1992, 2012 and 2018 but have never been sufficient to offset the risk of current and future claims. A 2010 provincial review concluded that assessments would have to rise 800 percent to achieve sustainability.

Chronically underfunded, the PBGF has skated past some big near-insolvencies, including Stelco and General Motors. This experience mirrors that of guarantee funds around the world: as a 2007 OECD study dryly noted, “Pension benefit guarantee schemes do not come without their difficulties.”

When things go wrong with pensions, they tend to go very wrong. PBGF assets have not always been sufficient to pay for claims, necessitating loans from the Consolidated Revenue Fund including $22 million for Massey Ferguson in 1988, $330 million for Algoma Steel in 2002 and $500 million for Nortel in 2010; all covering a risky open-ended public guarantee of private contracts.

The PBGF has featured in four reports since 1991, when the Pension Commission of Ontario expressed concern regarding its viability after the Massey insolvency. The 2008 OECP report recommended that a separate agency be established to operate the PBGF and charge cost-recovery premiums based on insurance principles. The 2010 review recommended substantial premium increases. The 2012 Drummond Commission report identified the PBGF as “a large fiscal risk” and recommended it be terminated or “transferred to a private insurer.”

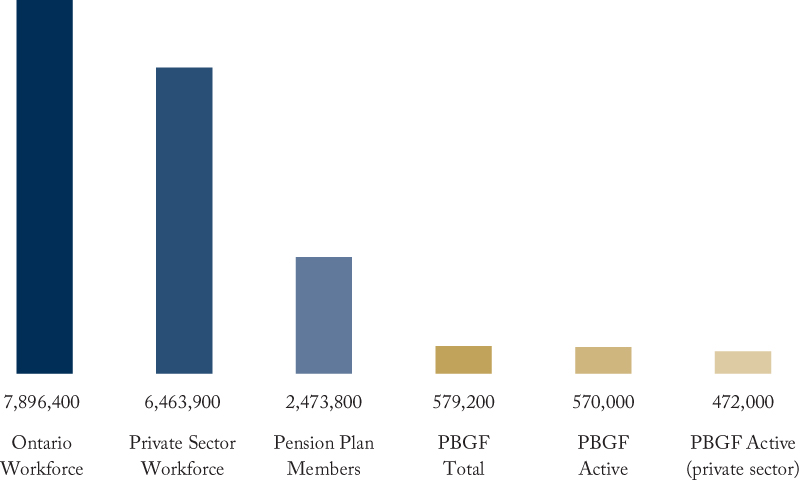

Having survived some existential crises, the PBGF remains underfunded (albeit modestly solvent) with net assets of about $900 million. With total loans of less than $1 billion over its 40-year history, Ontario taxpayers are fortunate the PBGF did not become the financial disaster that some reasonably feared it could have been. Nor does it appear likely to. PBGF risks decline in step with an inexorable, secular decline in DB pension plan membership. From 2010 to 2019, pension plan members with PBGF-guaranteed benefits declined from 1.1 million to about 580,000. Of that number, about 100,000 are in the public sector, winding-up or inactive plans which means that PBGF coverage in active plans applies to fewer than 500,000 members of Ontario’s private-sector workforce of 6.5 million (see Figure 1).

Figure 1

Source: Author’s calculations and other information presented are based primarily on 2019 data available online from Statistics Canada and the Financial Services Regulatory Authority of Ontario.

Better pension funding means less exposure for the PBGF. At the end of 2019, the projected median solvency funded ratio of Ontario DB plans was 99 percent (close to its 10-year high) with nine out of 10 plans over 85 percent funded. One could argue the PBGF now poses comparatively little risk: pension plans are well-funded; membership is low and falling; premiums have more than doubled; the fund is carrying a decent float. Perhaps most importantly, inflation has eroded the real value of PBGF coverage by half. And PBGF only covers about 7 percent of the workforce.

This is not to suggest that the PBGF guarantee amount should be increased or its scope expanded – the elimination of pension solvency funding in 2018 would make that especially risky. The Ontario government may wish to consider simply accepting its good fortune and direct its attention on the pension policy file to other, less risky and more useful initiatives, such as exploring practical ways to support and expand workplace pension coverage.

The 2020 Ontario Budget announced a review of the PBGF, as required by the Pension Benefits Act. Obvious questions that will arise include whether the PBGF should continue and, if so, how it can become more relevant to the majority of Ontario workers who have no pensions to guarantee. Notwithstanding 30 years of hand-wringing, one thing is clear: risks posed by the PBGF to Ontario’s finances have declined substantially, and will continue to do so. We still need better information about PBGF risk, however. Annual reports do not contain financial data on the amount of PBGF-covered pension liabilities and the degree to which such liabilities are funded. They should, and a sustainability analysis should be part of the Queen’s Park review.

With that said, it’s evident that risks are at an historic low. Clearly, one viable policy option is simply to let the venerable PBGF live out the rest of its days in tranquility. To the extent the government wants to get into the pension business, more ambitious plans might see it converted to a pension agency for stranded pension assets and low-price manager of funds for members of underfunded plans.

Whatever course the government chooses, it can breathe a sigh of relief that the PGBF is no longer the albatross it once appeared to be.

James Pierlot is the Founder and CEO of Blue Pier™ and a member of the C.D. Howe Institute Pension Policy Council.

To send a comment or leave feedback, email C.D. Howe at blog@cdhowe.org.

The views expressed here are those of the author. The C.D. Howe Institute does not take corporate positions on policy matters.

Original Source: https://www.cdhowe.org/intelligence-memos/james-pierlot-%E2%80%93-ontario%E2%80%99s-pension-benefits-guarantee-fund-practical-way-forward