You’ve heard of pension plans. You may even know a few people who have one. Probably, you already know that people with good pension plans retire better. A lot better. If you are a sole proprietor, a self-employed professional, or a business owner seeking a better financial future for yourself, a personal pension plan solution might be your best option.

Discover the power of a pension plan. You’ve seen others reap the rewards, and now it’s your turn. As a self-employed professional or business owner with a packed schedule, you need a straightforward plan that’s easy to understand and personalized for you. You need a plan that will stay with you for life – or let you leave easily if you need a change.

Get the inside scoop on the personal pension options available out there and see why Blue Pier’s™ “Personal” Pension Plan as a Service outshines RRSPs and the rest. It’s time to secure your future, effortlessly.

When choosing a personal pension plan provider, everyone should ask these questions:

| Blue Pierᵀᴹ | RRSP | Defined Benefit IPP | Defined Benefit MEPP | |

|---|---|---|---|---|

| Flexible retirement-income options | ✓ | ✗ | ✗ | ✗ |

| Tax-free portability | ✓ | ✓ | ✗ | ✗ |

| Low fees | ✓ | Depends | ✗ | Depends |

| Low Workload/Risk | ✓ | ✗ | ✗ | ✓ |

As a dedicated self-employed professional or business owner, we understand that your time is precious. You deserve a pension plan that effortlessly supports your financial future while you focus on the needs of your patients, clients, or other stakeholders. You probably don’t want complicated schemes and sleepless nights worrying whether you overplayed the rules or locked yourself into the wrong long-term commitment. With Blue Pier™ you can trust in a low-maintenance, gimmick-free plan that simply gets the job done right.

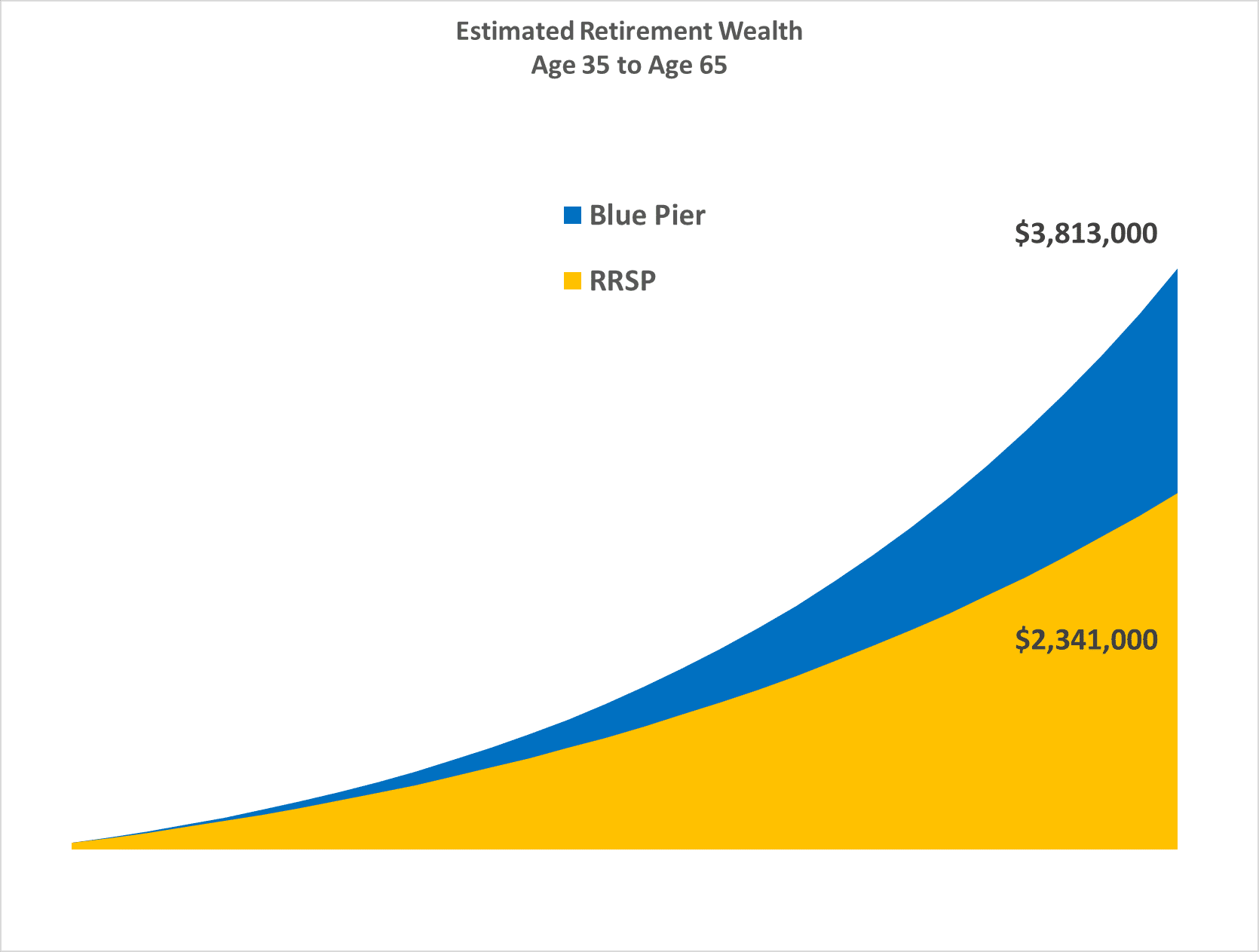

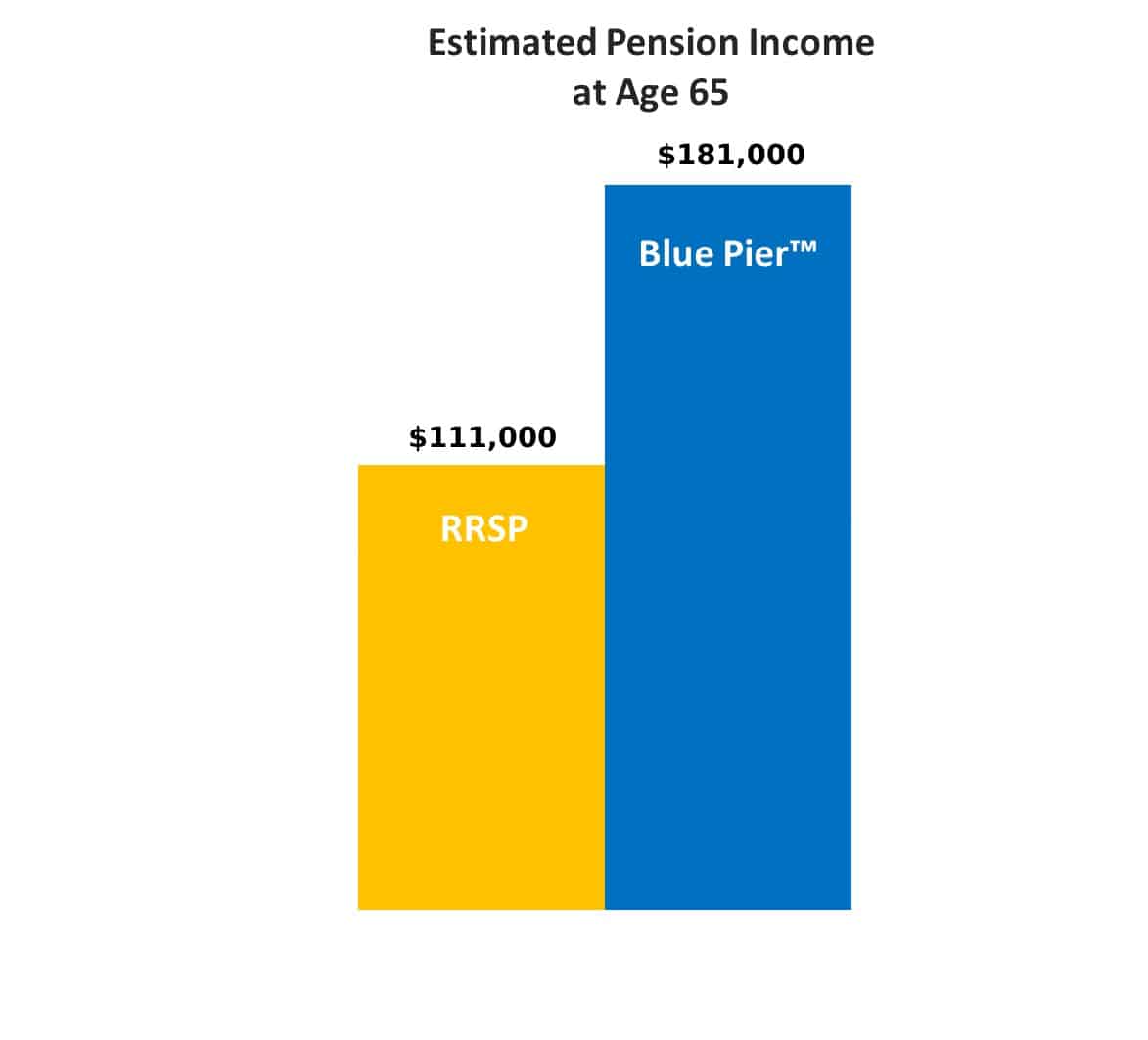

How much better can you retire? Look at the numbers and discover why Blue Pier™ may be a good fit for you. Rest easy, knowing you’ve played by the rules and secured your financial future.

*Assumptions provided on request. The projections shown above are intended to be used solely for illustrative and informational purposes. They are not a guarantee or a promise of performance.

In 10 weeks or less, you can have your own personal pension plan. Here’s how it works:

It’s that easy!

Don’t leave your retirement to chance. Book a free consultation or get in touch with Blue Pier™ today to start planning your personalized pension solution. Experience the peace of mind that comes with a pension plan designed exclusively for professionals like you. Trust in Blue Pier™ to guide you towards a worry-free and financially rewarding retirement.

Disclaimer: The information provided here is for informational purposes only and should not be considered as personalized financial advice. When evaluating your options for pensions, Blue Pier™ recommends consulting with a licensed, fee-only financial planner so you get independent, unbiased advice.